- June 08, 2015 by Jeanette Boleantu

The Expatriate Group strongly recommends that appropriate tax advice be sought prior to the withdrawal of any RRSP balances. There are two tax consequences that exist for withdrawing registered products before you retire –regardless of your tax residency status.

- The amount you redeem is taxable income: You have to report the amount you take out as part of your worldwide income. At that time, you may have to pay more tax on the money — on top of the withholding tax. It depends on your total income and tax situation.

- You pay a withholding tax: As a non-resident when you redeem RSP there is a 25% withholding tax that is due to CRA. This withholding tax is the NON-RESIDENT TAX LIABILITY on the income received. If a lower amount than 25% is withheld at source or a T3 slip is issued you need to file and pay the difference.

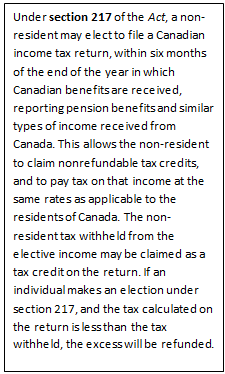

The financial institution will issue an NR4 notifying tax withheld at source in order to avoid filing a tax return as a non-resident. The Section 217 election allows a non-resident to voluntarily file a tax return so that they will have the same tax obligation as if they were a resident of Canada. This is a hassle and we do not recommend doing this. The only time a non-resident should file with CRA is if they received a T3 slip as a result of not changing their residency status on the address maintained with their financial institution.

Before you decide to withdraw your RRSPs, make sure that you consider all of your options. Consult with a

knowledgeable financial professional who can help you figure out the best way to go about making your withdrawals, and who can help you plan for your tax payments. Canadian tax regulations may provide relief from tax and penalties provided that the appropriate tax forms are filed with the CRA. For this reason

knowledgeable financial professional who can help you figure out the best way to go about making your withdrawals, and who can help you plan for your tax payments. Canadian tax regulations may provide relief from tax and penalties provided that the appropriate tax forms are filed with the CRA. For this reasonThe following illustrates the standard amount withheld for Canadian tax residents.

Non-Resident Tax Calculator – Results

Country of residence: Malaysia

Calculation date: 2015-06-05

Income type 1 from Canadian sources: RRSP/RRIF – Lump Sum Payment

Income amount: CAD $ 14,000.00

Tax rate: 25.0 %

Amount payable: CAD $ 3,500.00

Minus tax amount already deducted: CAD $ 0.00

Balance owing: CAD $ 3,500.00

Mobility Transition Coaching